Abstract

Over the past four decades, the role of the Chief Financial Officer (CFO) has evolved beyond traditional boundaries of accounting and compliance to become a central force in corporate strategy, digital transformation, and organizational leadership. Building on the concepts introduced in “The Rise of Strategic Modern Finance” this article examines the evolution of the CFO’s skill set—both hard and soft skills—that has redefined what it means to lead finance in the modern enterprise.

The article explores how analytical precision now coexists with emotional intelligence, and how data-driven insights converge with human-centered leadership. It highlights the competencies that have emerged over the last few decades and anticipates those that will shape the next generation of finance leaders. Drawing on research conducted by leading consulting firms and academic literature, this piece invites readers to reflect on the transformation of the CFO from merely being a financial steward to becoming a strategic orchestrator. It also provides a glimpse into the potential future of finance in an era characterized by intelligent, purpose-driven practices.

1. Introduction: A Profession in Constant Reinvention

Few executive roles have transformed as profoundly as that of the Chief Financial Officer. Initially perceived as the organization’s financial custodian, responsible for safeguarding accuracy, compliance, and cost control, the modern CFO has evolved into a strategic architect of performance, innovation, and growth. In today’s dynamic landscape, finance has transcended its traditional function of merely recording past transactions; it now plays a pivotal role in shaping the future.

This transformation is not solely due to technological advancements and data analytics; it also highlights the importance of people. As automation, artificial intelligence, and data-driven forecasting redefine the finance function, the ability to attract, develop, and inspire talent is as vital as mastering new tools.

According to Deloitte’s CFO Signals survey (2024), almost half of CFOs (47%) view talent—especially hiring and retention—as one of their top internal risks, second only to challenges related to generative artificial intelligence (GenAI) and the shortage of professionals ready to work in this area. This finding emphasizes a key point: the strategic evolution of finance relies heavily on its human resources, not just its digital capabilities.

In today’s finance landscape, leaders must adeptly balance technological skills with human empathy. To succeed, CFOs need to interpret complex data while also building teams capable of creative problem-solving, ethical decision-making, and adaptability. This combination of analytical precision and emotional intelligence lies at the heart of modern finance. Together, these elements reinforce one another, ultimately helping to create more resilient and forward-thinking organizations.

2. The Evolution of CFO Competencies: From Institutional Guardians to Strategic Orchestrators

The transformation of the Chief Financial Officer (CFO) role has been one of the most emblematic examples of how organizational functions evolve in response to economic, technological, and societal change. Rather than a linear timeline divided by decades, this evolution reflects a progressive broadening of competencies, shifting from control and stewardship toward strategy, digital fluency, and people leadership.

2.1 Institutional Roots and the Historical Evolution of the CFO Function

The role of the Chief Financial Officer (CFO) as a vital corporate figure has a rich historical evolution. Berland, Légalais, and Redon (2019) explore this development, highlighting how, during the postwar expansion of industrial capitalism, financial directors transitioned from being mere administrative accountants to influential decision-makers as companies grew more complex.

Furthermore, Lescure (2019) argues that the rise of the CFO represented a fundamental shift in corporate governance, linking financial expertise to strategic oversight and effective communication with investors.

As firms began to globalize in the late 20th century, the finance function became essential for coordinating resources, managing performance, and acting as a bridge between operational managers and capital markets (Sion, Bachy & Brault, 2014). As a result, the CFO took on the role of a strategic interpreter, balancing compliance responsibilities with a focus on future guidance.

Building on this historical foundation, the rise of integrated systems and data-driven management transformed how finance professionals operated within organizations.

2.2 The Hybridization of Financial Competence

The digital and organizational transformations of the early 21st century redefined the boundaries of finance expertise. Caglio (2003) introduced the concept of hybridization, explaining how enterprise resource planning (ERP) systems required accountants and finance leaders to integrate technical, technological, and relational skills. Granlund and Lukka (1997) further elaborated on this shift, describing the evolution of finance professionals from “bean-counters” to “change agents.” They noted that these individuals moved away from purely transactional control towards influencing strategy and fostering innovation.

These developments marked a significant transition for Chief Financial Officers (CFOs), who evolved from specializing in functional areas to focusing on cross-functional integration. In this new role, technical proficiency in analytics and systems became essential for effective leadership, communication, and adaptability.

2.3 From Competence to Capability: The Modern Frameworks

Modern professional organizations have recognized the importance of a dual skill set for finance professionals. The CIMA CGMA Competency Framework (2019) and the IMA Management Accounting Competency Framework (2019) both present a comprehensive view of professional capabilities. They emphasize that finance is a discipline that combines technical expertise—such as decision analysis, reporting, and risk management—with essential skills like communication, ethical judgment, and leadership.

Similarly, the IFAC (2002) Role of the CFO statement highlights that financial leaders should “create value through insight and influence,” rather than merely report it. This perspective is echoed in the recent IFAC PAIB guidelines, which stress the importance of digital agility and people development.

In academic literature, Maas and Matejka (2009) demonstrated how a CFO’s leadership style directly impacts the pace of management accounting innovation. They found that behavioral competencies—such as trust, openness, and a willingness to embrace change—are just as crucial for finance transformation as technical systems or analytical models.

Recent empirical research, including a study by Halima (2025), supports this view. It shows that the modern CFO operates within a hybrid finance model that integrates digital intelligence with human-centered leadership. This approach combines analytics, ethics, and emotional intelligence to drive strategic value creation.

2.4 Toward a Unified Competency Perspective

When taken together, these works highlight a consistent trend: the role of the CFO has evolved not only in how finance is managed but also in how leadership itself is conceived.

Today’s finance leaders are moving beyond traditional roles to incorporate elements such as institutional legitimacy and digital orchestration. Their skill set has expanded from merely ensuring compliance to fostering collaboration by bridging technical expertise, strategic insight, and human capability development.

This integration serves as the foundation for the competency matrix outlined in the next section, where hard and soft skills converge as complementary forces in shaping the finance leaders of the future.

While history explains how the CFO role expanded, modern frameworks reveal how its competencies have become codified and institutionalized.

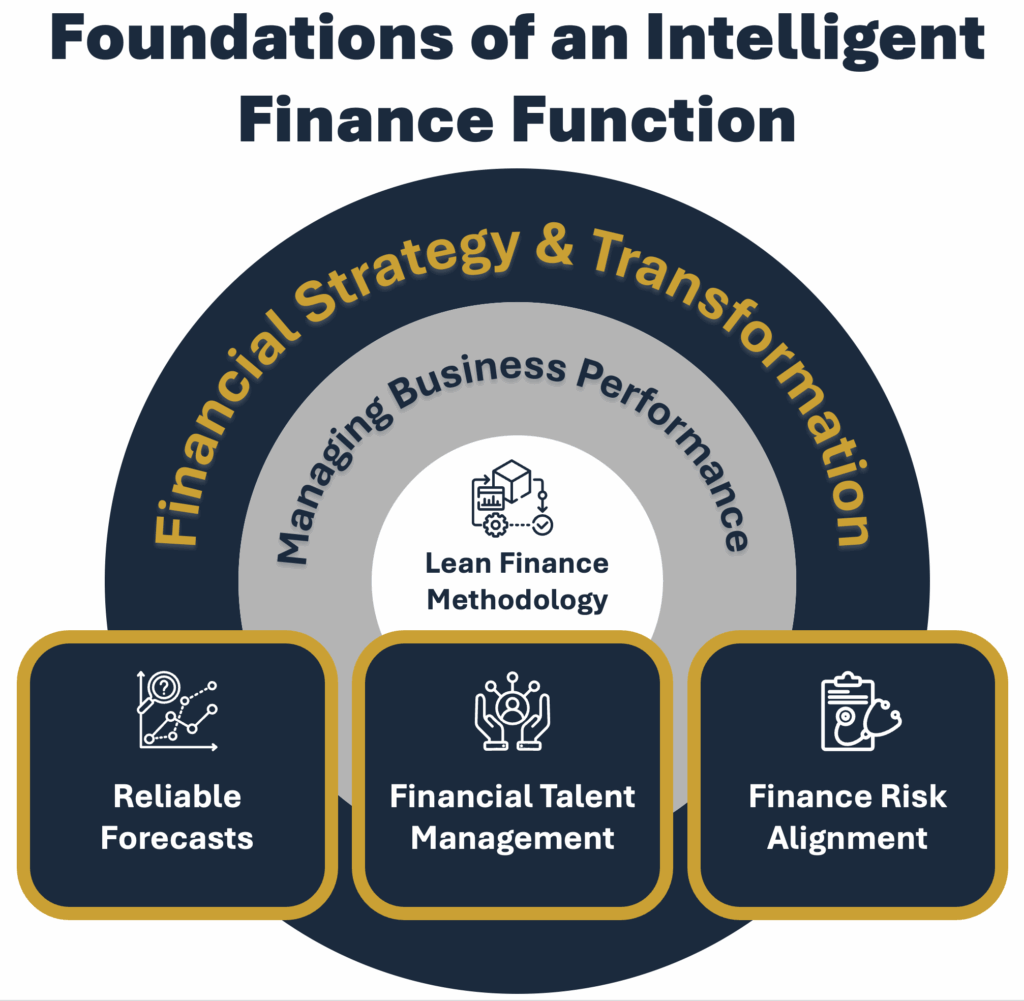

This evolution toward a unified and adaptive finance function can be visualized through the Foundations of an Intelligent Finance Function model (Figure 1).

The framework, adapted from Halima (2025) and Wensveen & Lepeak (2013), illustrates how financial strategy and transformation rest on three interdependent pillars: reliable forecasts, financial talent management, and finance–risk alignment—all supported by lean finance methodology. Together, these dimensions represent the operational and human foundations that enable strategic orchestration in modern finance.

Source: Adapted from Halima (2025), based on Wensveen & Lepeak (2013).

3. The New Competency Matrix: Integrating Technical Mastery and Human Capability

If Section 2 outlined the expansion of the CFO’s responsibilities over the decades and across various disciplines, the next question is: what combination of competencies defines the modern, integrated finance leader?

Current frameworks from global professional organizations—particularly CIMA, IMA, and IFAC—have converged on a comprehensive understanding of financial leadership. These frameworks emphasize that the value of the finance function lies not only in its outputs but also in its ability to facilitate decision-making, foster collaboration, and drive transformation throughout the organization.

3.1 The Foundation: Core Competency Domains

The CIMA CGMA Competency Framework (2019) identifies four core domains essential to contemporary financial leadership:

- Technical Skills – the analytical and accounting foundation that ensures the integrity of reporting, planning, and risk management.

- Business Skills – the ability to translate financial data into commercial insight, linking numbers to strategy and value creation.

- People Skills – communication, collaboration, and team leadership to influence across functions.

- Leadership Skills – vision, integrity, and agility to inspire trust and drive performance in uncertain contexts.

CIMA explicitly frames these dimensions as mutually reinforcing, emphasizing that the relevance of each fluctuates according to organizational maturity, industry dynamics, and transformation stage.

Similarly, the IMA Management Accounting Competency Framework (2019) presents five integrated pillars: Strategy, Planning and Performance; Reporting and Control; Technology and Analytics; Business Acumen and Operations; and Leadership. It introduces the concept of adaptive proficiency — the CFO’s ability to balance technical mastery with interpersonal and ethical judgment, scaling competencies as business needs evolve.

The IFAC PAIB Committee (2002, 2013) complements these models by articulating three overarching capabilities for finance professionals:

- Professional expertise – mastery of finance, accounting, and governance.

- Business acumen – understanding of value drivers and strategic alignment.

- People and leadership capability – fostering collaboration, ethical culture, and organizational resilience.

Together, these bodies reinforce the same message: finance leadership is not a static list of skills but a living system of interdependent competencies.

3.2 The Integrated CFO Competency Matrix

This matrix represents a balanced model in which hard and soft skills intersect dynamically. Technical expertise provides credibility; business acumen drives relevance; and leadership, ethics, and adaptability ensure sustainability. However, each organization must evaluate these competencies differently according to its specific context—this principle is now central to advanced leadership thinking.

| Competency Dimension | Core Components | Derived from | Application in Modern Finance |

|---|---|---|---|

| Technical and Analytical Mastery | Accounting, financial control, reporting standards, risk management, data analytics, and emerging digital tools. | CIMA (Technical), IMA (Reporting & Technology), IFAC (Professional Expertise) | Ensures integrity and transparency in decision-making; foundation for automation and AI adoption. |

| Strategic and Commercial Acumen | Strategic planning, performance management, capital allocation, scenario modeling, market insight. | CIMA (Business), IMA (Strategy & Performance), IFAC (Business Acumen) | Enables CFOs to act as co-pilots to the CEO, linking financial insight to enterprise value. |

| Leadership and People Development | Coaching, communication, team empowerment, succession planning, inclusion, ethical judgment. | CIMA (People & Leadership), IMA (Leadership), IFAC (People Capability) | Builds resilient teams and promotes cross-functional collaboration; key for transformation execution. |

| Digital and Innovation Fluency | Digital literacy, process automation, AI integration, innovation mindset. | CIMA (Digital Leadership), IMA (Technology & Analytics) | Positions finance as an enabler of efficiency and foresight. |

| Societal and Ethical Stewardship | ESG integration, sustainability metrics, stakeholder engagement, integrity. | IFAC (Ethics & Values), CIMA (Purpose & Sustainability) | Expands finance’s accountability beyond shareholders to broader stakeholders. |

Looking ahead, research such as Gartner’s “Finance Reimagined 2030” underscores that the finance function is entering an era where technology enhances human capabilities rather than replacing them. Gartner predicts that over 70 percent of financial decisions will be AI-assisted by the next decade. However, it emphasizes that human judgment, ethical reasoning, and contextual interpretation will remain the key differentiators (Gartner, 2023). This forecast reinforces that the future CFO must not only master digital tools but also embody the leadership, curiosity, and integrity that ensure technology serves as a source of insight rather than a replacement for human input.

In this context, the CFO of tomorrow will function at the intersection of technology, sustainability, and human development— orchestrating data intelligence, ethical purpose, and adaptive leadership to build resilient organizations and create responsible value.

3.3 Contextual Relevance and Situational Leadership Fit

The practical reality, as highlighted by Egon Zehnder (2022) in “The New Playbook of CFOs”, is that a CFO’s effectiveness depends on situational alignment. The “four archetypes” identified—Super Controller, Operational/Transformational, Corporate Strategist, and Externally Focused CFO—represent different contextual modes rather than fixed personalities. The significance of each archetype, and therefore each competency, varies depending on the company’s strategic phase: stabilization, growth, transformation, or capital-market expansion.

This concept aligns with contingency leadership theory (Fiedler, 1967) and dynamic capabilities theory (Teece et al., 1997), which suggest that leadership effectiveness stems not from rigid expertise but from the ability to adapt skills in response to changing environments. Consequently, the modern CFO is not just multi-skilled; they are responsive to context.

Therefore, when building a finance succession pipeline, it is important to emphasize learning agility and adaptability alongside technical development. Future-ready organizations will nurture leaders who can navigate fluidly across different archetypes, balancing hard and soft skills based on the situation. This situational adaptability is the defining characteristic of finance leadership today and serves as a bridge between the structured competency models of CIMA, IMA, and IFAC and the complex realities of today’s global business landscape.

4. Conclusion: The Adaptive Human at the Core of Financial Leadership

The evolution of the Chief Financial Officer (CFO) mirrors the transformation of modern organizations themselves. These organizations have transitioned from structures built on control and compliance to ecosystems driven by data, insight, and human capability. What once defined the CFO as a guardian of accuracy and efficiency has expanded into a multidimensional role that blends strategic foresight, digital fluency, and emotional intelligence. The journey from financial stewardship to strategic orchestration has been marked by a recurring pattern: progress in finance has always required progress in people.

Institutional studies, such as those by Berland et al. (2019) and Lescure (2019), and frameworks developed by CIMA, IMA, and IFAC, reveal that technical mastery alone no longer guarantees leadership relevance. Instead, effectiveness arises from the ability to balance analytical rigor with the softer, human dimensions of communication, empathy, and adaptability. These competencies are not opposites; they are complementary forces within a single continuum of value creation.

However, as the Egon Zehnder (2022) model reminds us, leadership success is never absolute. The CFO who excels in a transformation context may need to recalibrate when guiding a mature business through stability or expansion. The situational weight of each skill—hard or soft—shifts with the organization’s moment, strategy, and cultural maturity. This contextual agility is now the defining capability of modern finance leadership.

Ultimately, finance leadership has evolved from stewardship to strategic orchestration — a dynamic balance between digital intelligence and human insight. The organizations that cultivate such adaptive, human-centered financial leaders will not only navigate change but orchestrate it.

In this light, the most enduring competitive advantage of any organization will not be its algorithms or analytics but its ability to develop adaptive, human-centered financial leaders—professionals capable of navigating change, empowering teams, and reimagining value creation in an ever-evolving world.

5. References

Berland, N., Légalais, L., & Redon, M. (2019). L’évolution du métier de directeur financier : origines, compétences, trajectoires. Entreprises et Histoire, 2(95), 55–71. https://doi.org/10.3917/eh.095.0055

Caglio, A. (2003). Enterprise Resource Planning Systems and Accountants: Toward Hybridization? European Accounting Review, 12(1), 123–153. https://doi.org/10.1080/0963818031000087853

Chartered Institute of Management Accountants (CIMA). (2019). CGMA Competency Framework: Finance Leadership in a Digital World. https://www.cgma.org/resources/tools/cgma-competency-framework.html

Deloitte. (2024). CFO Signals: Q2 2024 survey results. Deloitte Development LLC. https://www.deloitte.com/us/en/programs/chief-financial-officer/articles/cfo-signals-2q-2024.html

Egon Zehnder (2022). The New Playbook of CFOs.

Fiedler, F. E. (1967). A Theory of Leadership Effectiveness. New York: McGraw-Hill.

Gartner. (2023). Finance Reimagined 2030: The Future of Decision Making. Gartner Inc.

Granlund, M., & Lukka, K. (1997). From Bean-Counters to Change Agents: The Finnish Management Accounting Culture in Transition. LTA, 3(97), 213–255.

Halima, H. (2025). Financial Analysis in the Digital Era: Transforming CFO Profiles and the Roles of Finance Functions. Brazilian Journal of Business, 7(2), –.

Hersey, P., & Blanchard, K. H. (1969). Life Cycle Theory of Leadership. Training and Development Journal, 23(5), 26–34.

Institute of Management Accountants (IMA). (2019). Management Accounting Competency Framework. Montvale, NJ: IMA. https://www.imanet.org/-/media/imasite/about-ima/management-accounting-competency-framework.pdf

International Federation of Accountants (IFAC). (2002). The Role of the Chief Financial Officer. New York: IFAC. https://www.ifac.org

International Federation of Accountants (IFAC PAIB). (2013). The role of the CFO: A global debate on preparing accountants for finance leadership. https://www.ifac.org

IFAC PAIB Committee (2013). The Role of the CFO: A Global Debate on Preparing Accountants for Finance Leadership.

Korn Ferry. (2022). CFO of the Future: Leadership Competencies in a Digital World. Korn Ferry Institute.

Lescure, M. (2019). De la fonction financière à la direction financière. Entreprises et Histoire, 2(95), 5–15.

Maas, V. S., & Matejka, M. (2009). How CFOs Determine Management Accounting Innovation: An Examination of Direct and Indirect Effects. European Accounting Review, 18(4), 667–695.

Sion, M., Bachy, B., & Brault, D. (2014). Profession Directeur Financier : Relever les défis techniques et managériaux de la fonction. Paris: Dunod.

Teece, D. J., Pisano, G., & Shuen, A. (1997). Dynamic Capabilities and Strategic Management. Strategic Management Journal, 18(7), 509–533.