At the turn of the 21st century, the finance function in corporations was largely perceived as a support role—responsible for reporting, budgeting, and ensuring regulatory compliance. Historically rooted in stewardship, compliance, and transactional support, finance professionals were expected to maintain the integrity of financial records and support statutory obligations (Chappuis, Kim & Roche, 2008).

In academia, the primary focus remained on capital structure decisions, rooted in foundational theories like Modigliani and Miller’s (1958) capital structure irrelevance proposition and Jensen and Meckling’s (1976) agency theory. While these models are crucial for understanding investor behavior and financial markets, they offer limited guidance on the internal, day-to-day managerial role of finance. Even classical finance textbooks, such as Gitman’s Principles of Managerial Finance and Ross’s Corporate Finance, typically devote little attention to the organizational positioning of finance or its contribution to operational decision-making. In contrast, Chang (2014) proposed a modern framework distinguishing between three distinct roles of finance: scorekeeper, guardian, and strategic advisor. This approach provides a more nuanced and actionable lens through which to assess the evolving expectations placed on finance professionals, especially as organizations increasingly rely on finance not only to report performance but also to help shape it.

The 2008 global financial crisis marked a pivotal moment. Beyond the immediate challenges of liquidity and solvency, it revealed the limitations of conventional risk and performance measurement models. As documented in studies by McKinsey and others, finance leaders were compelled to reevaluate decision-making under uncertainty, leading to an accelerated push for greater transparency, scenario analysis, and integrated forecasting (Chappuis, Kim & Roche, 2008). The crisis’s aftermath prompted a shift from reactive finance to a more proactive, value-driven function—one that not only reports financial outcomes but also shapes business strategy.

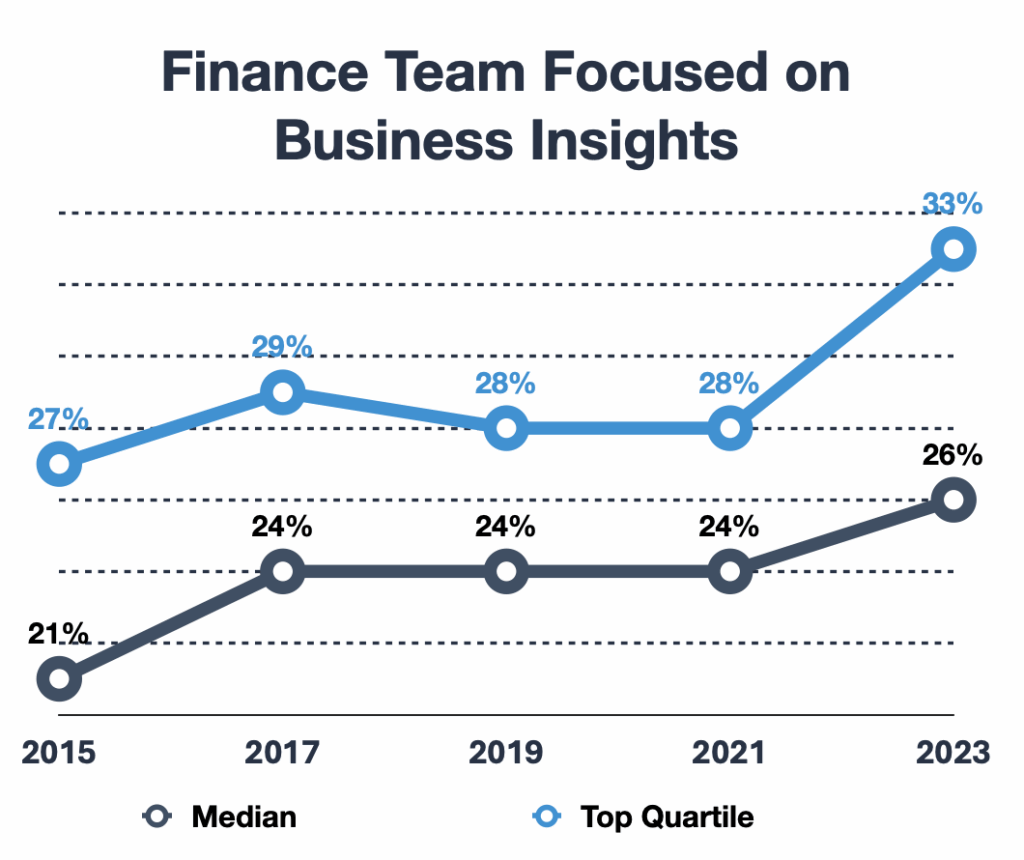

According to Chang (2014), this transition reflected an emerging “Strategic Finance” paradigm, in which finance professionals are increasingly expected to contribute to long-term planning, capital allocation, and competitive differentiation. This evolution is not simply about enhanced analytical capabilities, but about finance occupying a central role in strategic decision-making processes. In other words, finance shifted from value reporting to value orchestration. This shift is empirically supported by recent data (see Figure 1), showing that top-performing finance functions now dedicate over 33% of their capacity to business-facing activities—up from 27% in 2015.

In parallel, large-scale surveys—such as IBM’s Value Integrators study (2010)—identified high-performing CFOs who excelled in integrating financial insights into strategic initiatives. These organizations outperformed peers in metrics such as revenue growth, EBITDA, and ROIC, reinforcing the financial upside of a strategic finance orientation. Yet the transformation was uneven. Kambil (2011) noted that although CFOs aspired to spend up to 60% of their time on strategic matters, most devoted less than half, often due to talent gaps, legacy systems, and cultural inertia.

The second major transformation emerged with the data revolution of the 2010s. Digital technologies, including ERP systems and Business Intelligence (BI) platforms, enabled the collection, storage, and analysis of vast amounts of financial and operational data. This led to a blurring of the lines between finance, IT, and operations. Consequently, finance professionals needed to develop hybrid capabilities, including financial acumen, data literacy, and strategic thinking, to meet the demands of this new era.

The global COVID-19 pandemic further reinforced this shift. Organizations that had invested in finance transformation—particularly digital automation and agile planning—proved more resilient in adapting to demand shocks and supply chain disruptions. As a result, CFOs have assumed increasingly strategic leadership roles, not only in financial stewardship but in business continuity, digital innovation, and stakeholder engagement. The pandemic era spotlighted the need for finance teams to operate with speed, agility, and insight, as real-time decisions around liquidity, supply chain viability, and market responsiveness became existential.

Beyond the pandemic, the post-2020 environment has been further shaped by escalating geopolitical tensions, trade disputes, and tariff realignments. These developments have introduced new layers of uncertainty in global supply chains, capital flows, and inflation dynamics. For CFOs, this heightened volatility has emphasized the importance of scenario planning, liquidity management, and geopolitical risk assessment. In this evolving landscape, finance leaders are increasingly expected to not only anticipate external shocks but to enable their organizations to respond with agility and foresight.

Building on this trend, Verbeeten (2025) argues that the 21st-century finance function is being redefined by digital fluency. He introduces the concept of “Finance 4.0,” which integrates automation, cloud computing, and artificial intelligence to elevate finance from operational efficiency to strategic foresight. Automation has reduced the need for human intervention in transactional tasks—such as reconciliations, journal entries, and routine reporting—allowing professionals to focus on forecasting, risk modeling, and scenario planning. More importantly, finance is increasingly expected to serve as a cross-functional integrator, linking commercial, operational, and technological domains through data-driven insights.

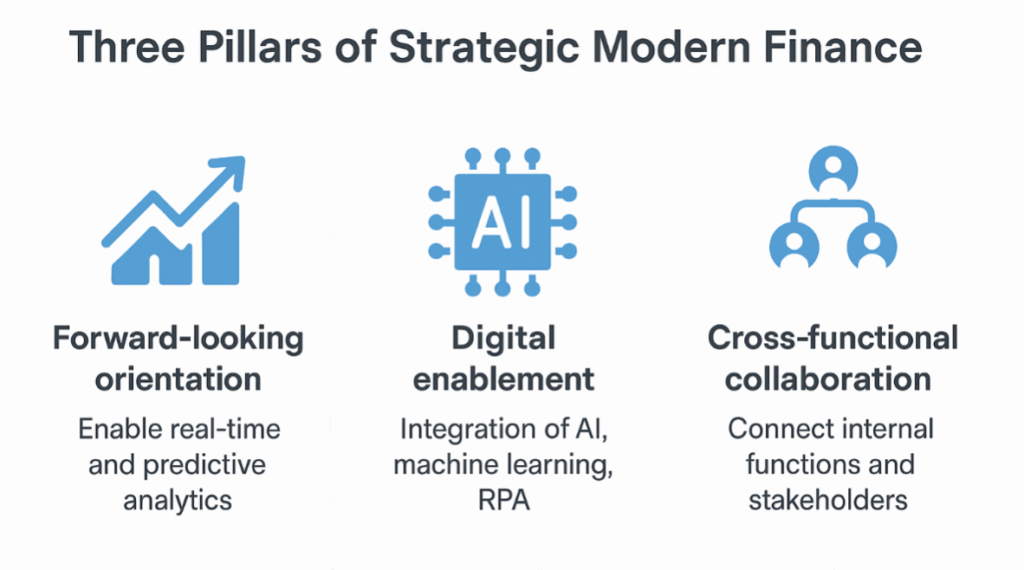

Today, Strategic Modern Finance can be defined by three key pillars:

- Forward-looking orientation: Modern finance moves beyond historical reporting to enable real-time and predictive analytics that inform strategic decisions.

- Digital enablement: The integration of AI, machine learning, RPA (Robotic Process Automation), and advanced analytics empowers finance to generate insights faster and more accurately.

- Cross-functional collaboration: Finance serves as a hub that connects internal functions—marketing, operations, supply chain, and HR—with external stakeholder expectations.

Looking ahead, the next frontier in finance will be shaped by Generative AI, sustainability reporting (ESG), and real-time strategic modeling. Gartner (2024) predicts that by 2026, more than 80% of finance teams in large enterprises will use AI-powered tools to augment forecasting and risk analysis. Similarly, McKinsey & Company (2021) notes that organizations that embed digital finance capabilities at the core of their decision-making process outperform peers by up to 20% in total shareholder return.

Yet, the transition to Strategic Modern Finance is not merely a matter of adopting new tools or technologies. It requires a fundamental rethinking of finance culture, organizational design, governance models, and the roles and capabilities of financial professionals. Studies such as KPMG’s CFO Agenda for Elevating Finance (2022) and PwC’s Finance Effectiveness Benchmark (2024) highlight that successful transformations blend automation with strategic upskilling, embedded analytics, and innovation management—emphasizing not only what finance does, but how it delivers value.

In this evolving environment, the modern finance leader must master a dual mandate: to safeguard the enterprise through robust controls and risk management, and to propel it forward through insight generation, strategic influence, and innovation leadership. Doing so requires navigating complex stakeholder dynamics, fostering cross-functional collaboration, developing data-driven decision frameworks, and building resilient and adaptive teams. These dimensions—spanning culture, technology, talent, leadership, and strategic integration—form the core of the evolving finance function and will be explored throughout the chapters ahead.

References:

Chang, R. (2014). Reframing the Role of Finance: Strategy Beyond Numbers. Strategic Finance Journal, 95(6), 45–51.

Chappuis, B., Kim, S., & Roche, T. (2008). Starting up as CFO. Available at: https://www.mckinsey.com/capabilities/strategy-and-corporate-finance/our-insights/starting-up-as-cfo

Gartner (2024). Gartner Predicts That 90% of Finance Functions will Deploy at Least One AI-enabled Technology Solution by 2026. Available at: https://www.gartner.com/en/newsroom/press-releases/2024-09-12-gartner-predicts-that-90-percent-of-finance-functions-will-deploy-at-least-one-ai-enabled-tech-solution-by-2026

IBM (2010). The New Value Integrator: Insights from the Global Chief Financial Officer Study. Available at: https://www.ibm.com/services/us/gbs/thoughtleadership/cfostudy

Jensen, M. C., & Meckling, W. H. (1976). Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure. Journal of Financial Economics, 3(4), 305–360.

Kambil, A. (2011). Crossing the chasm: From operator to strategist. Available at: https://www2.deloitte.com/us/en/insights/focus/executive-transitions/crossing-the-chasm-from-operator-to-strategist.html

KPMG (2022). CFO agenda for elevating finance. Available at: https://kpmg.com/us/en/articles/2023/cfo-agenda-for-elevating-finance.html

McKinsey & Company. (2021). Digital strategy in corporate finance: From operational to strategic excellence. https://www.mckinsey.com/capabilities/strategy-and-corporate-finance/our-insights/digital-strategy-in-corporate-finance-from-operational-to-strategic-excellence

Modigliani, F., & Miller, M. H. (1958). The Cost of Capital, Corporation Finance and the Theory of Investment. The American Economic Review, 48(3), 261–297.

PwC (2024). Becoming the Catalyst: How finance functions are driving shareholder value. 2024. Available at: https://www.pwc.com.br/pt/estudos/setores-atividades/financeiro/2024/PwC-2024-Finance-Effectiveness-Benchmarking-Study.pdf

Verbeeten, F. H.M. and Bedford, D. S., Derichs, D., Hoozée, S., Malmi, T., Messner, M., Sinha, VK, van der Kolk, B. (2025). Digitalization of the finance function: Automation, analytics, and finance function effectiveness. Management Accounting Research 67 (2025) 100942. http://dx.doi.org/10.2139/ssrn.4812512